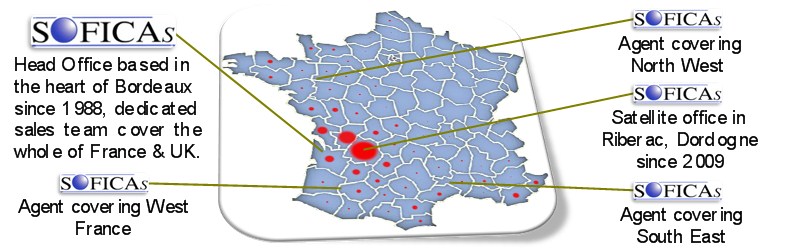

Partners

Health cover in France - A few definitions

rong>A FEW DEFINITIONSrong>

rong>

rong>

rong>

rong>

rong>

rong>

rong>

Understanding The French System:

rong>

rong>rong>

Unlike the English system, the French regime makes no difference between the public and private treatments

(the reimbursement rates are identical).

On the other-hand, the 'Sécurité Sociale' alone does not cover the entirety of your expenses.

rong style="text-align: center;">

rong style="text-align: center;">rong style="text-align: center;">First column represents the total cost of your medical treatment. rong>

rong>

rong style="text-align: center;">rong style="text-align: center;">

rong style="text-align: center;">Second column shows the possible reimbursements:

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange = reimbursable with minimum cover

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange to Red = Only reimbursable with higher cover or not at all.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Third column indicates where the reimbursements could come from.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Click on each column to see their individual definitions:

rong>

rong style="text-align: center;">rong>

rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>

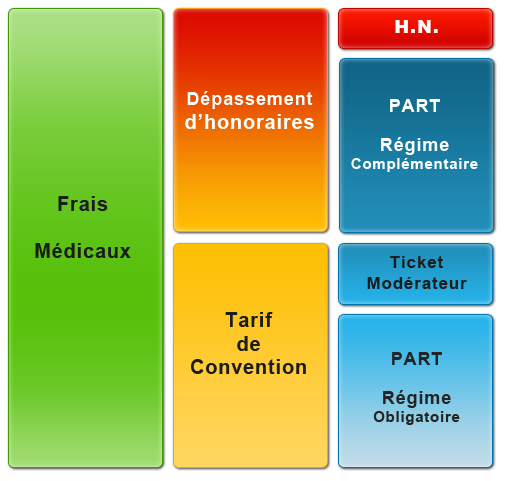

rong>Frais Médicauxrong> :

The TOTAL amount charged for your treatment.

This can be a Fixed rate or an amount announced by a specialist.

rong>Dépassement d'honorairesrong> :

Amount charged by a Doctor for time spent treating a patient.

A Doctor in "Secteur 1" will NOT charge over the"Tarif de Convention" and you will be totally reimbursed even on the lowest levels of Top-UP.

A Doctor in "Secteur 2" can charge over the "Tarif de Convention" and you will only be reimbursed if you have a higher level of "Top-Up".

You could be faced with "Dépassement d'honoraires" for a simple 15 minute Specialist visit or for 4 hours of Major Surgery.

Rates charged must be communicated in advance, get in contact with the administration if not. .

rong>Tarif de Conventionrong> :

Base rate given to medical treatment recognizable by a code that indicates its nature and tariff called “Nomenclature” fixed by the “CCAM”(Classification Commune des Actes Médicaux).

The “Tarif de Convention” fixes the 100% base rate that all medical professionals use but it does NOT limit their fees charged.

Top-Ups relate to the base rate and NOT to actual expenses. .

rong>Ticket modérateurrong> :

This represents the difference between your “Régime Obligatoire” reimbursements and the "Tarif de Convention".

This amount, normally reimbursed by a Top-Up will be reimbursed by your “Régime Obligatoire” in case of long-term illness, handicap or maternity.

The “100%” or the "TM" referred to on "Tiers Payant“ slips from Top-Ups will guarantee payment of the "Ticket Moderateur" to any professional accepting to use this facility without having to advance any money. .

rong>Part Régime Obligaroirerong> :

The Percentage of the "Tarif de Convention" that is covered by your “Régime Obligatoire”.

Usually these reimbursements come from "CPAM" or “RSI” if you are self employed.

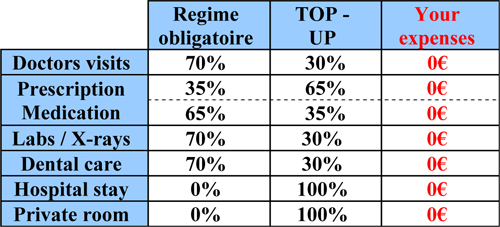

Reimbursements range from 35% to 100% but are commonly referred to as 70% of the "Tarif de Convention".

Once fully into the French system you will receive a “Carte Vitale”.

This card replaces payment to medical professionals equipped with the “System Noemi”.

rong>Part Régime Complémentairerong> :

"Part Mutuelle". This is the amount paid on your behalf by a Top-Up.

"Dépassement d'honoraires" can be reimbursed by a Top-Up.

Top-Ups starts at 100% and can go up to 600% or more depending on your needs and especially what area you live in.

SOFICA’s sugests middle cover, around 200% for hospitalization permitting you to use Doctors charging twice the "Tarif de Convention“ but lower for the rest as some base rates are very low.

rong>Hors Nomenclaturerong>:

These are treatments that are NOT included on the “CCAM” list thus they do not have a base rate.

These treatments are often in addition to ongoing treatment.

The “CCAM” tend to exclude preventative medicines, "Médecines douces“ that have not been accepted by the “Académie des Sciences”.

Some Top-Ups reimburse thing like osteopathy and homeopathy using Fixed rates set by the companies called “Forfait Annuel”.

rong>

rong>

rong>

Examples of reimbursement: rong>

rong> rong>

rong>rong>

rong> SOFICAS clients benifit fully from the French system  as we use French companies that know thier subject.rong>

as we use French companies that know thier subject.rong>

rong>rong>

"Télétransmition"

Automatic reimbursements using only your "Carte Vitale".

rong>rong>

"Tiers Payant"

No money to be advanced at the chemist / lab / x-ray and more.

rong>rong>

"Prise en charge"

Possible on demand even for Optical and Dentistry.

rong>rong>

Hospitals stay expenses can be paid directly by your "Top-Up".

"Frais de séjours and chambre particulière"

rong>

rong>

rong>rong>

rong>

Hospitalization / Hospitalisation:rong>

rong>rong>

rong>rong>

rong>The question of payment will come after your wellbeing

If you are in an emergency situation, you will be taken care of regardless of your nationality, professional or financial situation.

However, after this point or if you have a planned hospital stay you could be asked for a “PEC”.

This "PEC" enables the hospital or Clinique to claim amounts due for your treatments directly from your "Régime Obligatoire" and eventually your "TOP-UP".rong>

rong>rong>

rong>If you are in France on holiday you may present your “EHIC”.

You will be asked for your blood group card - "carte de groupe sanguin'".

They will ask about allergies - "avez-vous des allergies?" or "êtes-vous allergique?".

You will be asked for your medrong>rong style="color: #000000;">icarong>rong style="color: #000000;">l hirong>rong style="color: #000000;">story rong>rong style="color: #000000;">- "rong>rong style="color: red;">antécédents médicaux ou chirurgicrong>rong style="color: red;">auxrong>rong>".

rong>rong> You will be asked about any medication you are taking – "rong>rong style="color: #ff0000;">Quel est votre traitement actuel / courant/ en cours?rong>rong>"

rong>rong> They will ask about your diet – "rong>rong style="color: #ff0000;">Avez-vous un régime spécial?rong>rong>" Without salt – "rong>rong style="color: #ff0000;">Sans selrong>rong>" Without sugar – "rong>rong style="color: #ff0000;">Sans sucrerong>rong>" Gluten free – "rong>rong style="color: #ff0000;">Sans glutenrong>rong>"rong>

rong>rong>

rong>Key Words:rong>

|

rong>rong>

rong>rong>

rong>Useful Phrases:rong>

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Aching |

Douloureux |

| Ambulance |

Ambulance |

| Anaesthetic |

Anesthésique |

| Anaesthetic |

Anesthésie |

| Ankle |

La cheville |

| Appendix |

L'appendice |

| Arm |

Le bras |

| Assistant nurse |

Aide soignante |

| Back |

Le dos |

| Back of the neck |

La nuque |

| Bedpan |

Un bassin |

| Bell / buzzer |

Sonnette |

| Bladder |

La vessie |

| Blood |

Le sang |

| Blood test |

Prise de sang |

| Blood test (results) |

Résultat sanguin, Bilan sanguin |

| Blood test to be taken fasting |

Prise de sang à jeun |

| Body |

Le corps |

| Bone |

L'os |

| Bottle |

Une bouteille |

| Bowels |

Les intestins |

| Brain |

Le cerveau |

| Breast |

Le sein |

| Bruise |

Un bleu /une contusion / un hématome |

| Burn |

une brûlure |

| Burning sensation |

Sensation de chaleur / douleur cuisante |

| Buttocks / bottom |

Les fesses |

| Calf |

Le mollet |

| Capsule |

Gélule |

| Car accident |

Accident de la route |

| Casualty / A&E |

Urgences |

| Change your dressing |

Faire votre pansement |

| Cheeks |

Les joues |

| Chest |

La poitrine |

| Chin |

Le menton |

| Collarbone |

La clavicule |

| Contraceptive pill |

La pilule |

| Cough / a cough |

Tousser / une toux |

| Covered in bruised |

Etre couvert de bleus |

| Crushed |

Ecrasé / broyé |

| Crutches |

Les béquilles |

| Cut |

coupe |

| Dizziness |

le vertige |

| Doctor |

Médecin |

| Drawsheet |

L’alèse |

| Dressing gown |

robe de chambre |

| Drink (A) |

Une boisson |

| Drink (To) |

Boire |

| Ear |

L'oreille |

| Eat |

Manger |

| ECG |

Electrocardiogramme (électro) |

| Elbow |

Le coude |

| Exhausted |

épuisé |

| Eye (eyes) |

L’œil (Les yeux) |

| Face |

Le visage |

| Face flannel |

Un gant de toilette |

| Feel sick |

J'ai des nausées / J'ai mal au cœur |

| Feel unwell / faint |

J'ai un malaise / j'ai la tête qui tourne |

| Finger |

Le doigt |

| Fingernail |

L'ongle |

| Foot |

Le pied |

| Forehead |

Le front |

| Gall bladder |

La vésicule biliaire |

| Get undressed |

Déshabillez-vous |

| Grazed |

écorché |

| Gum |

Gencive |

| Hand |

La main |

| Have a wash |

Faire sa toilette |

| Head |

La tête |

| Heart |

Le cœur |

| Heel |

Le talon |

| High temperature |

la fièvre |

| Hip |

La hanche |

| Hospital gown (open at the back) |

Casaque / blouse opératoire |

| Infection |

Infection |

| Injection |

Piqûre |

| Intensive care |

Soins intensive |

| Jaw |

La mâchoire |

| Kidney |

Le rein |

| Knee |

Le genou |

| Liver |

Le foie |

| Lower back |

Les lombaires / les reins |

| Lungs |

Les poumons |

| Make the bed |

Faire le lit |

| Meal |

Un repas |

| Medicine (treatment) |

Médicament / traitement |

| Mouth |

La bouche |

| Muscle |

Le muscle |

| Nausea |

la nausée |

| Neck |

Le cou |

| Nightdress |

Chemise de nuit |

| Nose |

Le nez |

| Nurse |

Infirmière |

| Operating theatre |

Bloc opératoire |

| Operation |

Intervention chirurgicale |

| Operation |

Intervention |

| Out of breath |

essoufflé |

| Pain killer |

Calmant |

| Paramedics |

SAMU |

| Permission to operate |

Autorisation d’opérer |

| Physio after an accident |

Re-éducation |

| Physiotherapist |

Kinésithérapeute |

| Physiotherapy |

Kinésithérapie |

| Pill |

Cachet / Comprime |

| Pyjamas |

Pyjama |

| Rib |

La côte |

| Scratch |

une égratignure |

| Sensitive |

Sensible |

| Set up a drip |

Faire une perfusion |

| Shoulder |

L’épaule |

| Sleeping pill |

Somnifère |

| Slippers |

Pantoufles |

| Soap |

Le savon |

| Sore |

endolori |

| Spleen |

La rate |

| Sticking plaster |

Sparadrap / pansement adhésif |

| Stitches |

Points de suture |

| Stomach (external) |

Le ventre |

| Stomach (internal) |

L'estomac |

| Stretcher |

Brancard |

| Surgeon |

Chirurgien |

| Surgical dressing |

Pansement |

| Swelling |

une bosse |

| Swollen |

enfle |

| Take your blood pressure |

Contrôler votre tension |

| Teeth |

Les dents |

| Tender |

sensible |

| Tendon |

Le tendon |

| Thigh |

La cuisse |

| Throat |

La gorge |

| Thumb |

Le pouce |

| Tired |

fatigue |

| Toenail |

L'ongle du pied |

| Toes |

Les orteils |

| Tongue |

Le langue |

| Towel |

Une serviette |

| Ulcer |

ulcère |

| Water |

L'eau |

| Wheelchair |

Fauteuil roulant |

| Wounded |

blessé |

| Wrist |

Le poignet |

| X-ray |

Radio |

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Call an ambulance |

Appeler une ambulance |

| Call the emergency services |

Appeler le urgences |

| Call the police |

Appeler la police |

| Do not get up |

Ne pas se lever |

| Do you know an English speeking doctor? |

Connaissez-vous un médecin qui parle anglais? |

| Do you want an injection? |

Voulez-vous une piqûre? |

| I am allergic to… |

Je suis allergique a / a la / aux… |

| I am constipated |

Je suis constipé(e) |

| I am diabetic |

J'ai le diabète |

| I am going to faint |

Je vais m’evanouir |

| I am in pain |

J'ai mal |

| I am taking medication |

Je prends des médicament |

| I don't feel very well |

Je ne me sens pas tres bien |

| I feel better |

Je me sens mieux |

| I feel sick |

J'ai envie de vomir / J'ai mal au cœur |

| I feel bad |

Je me sens mal |

| I feel weak |

Je me sent faible |

| I feel worse |

Je me sens moins bien |

| I fell over |

Je suis tomber |

| I have a broken bone |

J’ai une fracture |

| I have a broken tooth |

J'ai une dent cassée |

| I have a chest cold |

J’ai une bronchite |

| I have a cold |

Je suis enrhumé |

| I have a cold |

J’ai une rhume |

| I have a got fever |

J’ai de la fievre |

| I have a headache |

J'ai mal à la tête |

| I have a sore throat / tonsilitis |

J'ai mal a la gorge / j'ai une angine |

| I have a wound |

J’ai une blessure |

| I have an abscess |

J'ai un abcès |

| I have an abscess |

J’ai un abcès |

| I have back ache |

J'ai mal au dos |

| I have been sick |

J'ai vomi |

| I have burnt myself |

Je me suis brûlé |

| I have chest pains |

J’ai des douleur à la poitrine |

| I have cut myself |

Je me suis coupé |

| I have flu |

J'ai la grippe |

| I have gor a head ache |

J’ai mal à la tête |

| I have got a headache |

J’ai mal à la tête |

| I have got a sore throat |

J’ai mal à la gorge |

| I have got a stomach ache |

J’ai mal à l’estomac |

| I have got cramps |

J’ai des cramps |

| I have got diarrhea |

J’ai la diarrhea |

| I have had a heart attack |

J’ai eu une crise cardiaque |

| I have lost a filling |

J'ai perdu un plombage |

| I have pain |

J'ai de la douleur |

| I have pains in the chest |

J'ai mal à la poitrine |

| I have shivers |

J’ai des frissons |

| I have stomach ache |

J'ai mal au ventre |

| I have the flu |

J’ai la grippe |

| I have to see a doctor |

J'ai dois de voir un médecin |

| I have toothache |

J'ai mal aux dents |

| I have wind |

J'ai des gaz |

| I need a bedpan |

J’ai besoin d'un bassin |

| I think it's broken |

Je pense que c'est cassé |

| I want a pee |

Je veux faire pipi |

| I'm bleeding |

Je saigne |

| I'm dizzy |

J’ai la vertige |

| I'm hungry |

J'ai faim |

| I'm sick |

Je suis malade |

| I'm sweating |

Je transpire |

| I'm thirsty |

J'ai soif |

| Is it serious? |

C’est grave? |

| It hurts everywhere |

J’ai mal partôut |

| It hurts here |

J’ai mal ici |

| It is painful since… |

C'est douloureux depuis… |

| Its swelling |

Ca enfle |

| I've been sick |

J'ai vomi |

| I've got the shivers |

J'ai des frissons |

| Permanent filling |

Obturation définitive |

| Stay lying down |

Restez allongé |

| Temporary filling |

Obturation provisoire |

| That hurts |

ça me fait Mal |

| That hurts! |

Ca me fait mal ! |

| That is very painful |

C'est très douloureux |

| That itches |

Ca me démange |

| That itches |

Ca me gratte |

| That tickles |

Ca me chatouille |

| That's too loose |

Ce n'est pas assez serré |

| That's too tight |

C'est trop serré |

| There has been an accident |

Il y a eu un accident |

| To have a bowel movement (phoo) |

Aller à la selle (faire caca) |

| To ring (for a nurse) |

Sonner l'infermiere |

| To urinate |

Uriner (faire pipi) |

| Where is the Chemist? |

Ou se trouve la pharmacie? |

| Where is the Doctors? |

Ou se trouve un medecin? |

| Where is the Hospital? |

Ou se trouve l'hôpital? |

|

Partners

Health cover in France - A few definitions

rong>A FEW DEFINITIONSrong>

rong>

rong>

rong>

rong>

rong>

rong>

rong>

Understanding The French System:

rong>

rong>rong>

Unlike the English system, the French regime makes no difference between the public and private treatments

(the reimbursement rates are identical).

On the other-hand, the 'Sécurité Sociale' alone does not cover the entirety of your expenses.

rong style="text-align: center;">

rong style="text-align: center;">rong style="text-align: center;">First column represents the total cost of your medical treatment. rong>

rong>

rong style="text-align: center;">rong style="text-align: center;">

rong style="text-align: center;">Second column shows the possible reimbursements:

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange = reimbursable with minimum cover

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange to Red = Only reimbursable with higher cover or not at all.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Third column indicates where the reimbursements could come from.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Click on each column to see their individual definitions:

rong>

rong style="text-align: center;">rong>

rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>

rong>Frais Médicauxrong> :

The TOTAL amount charged for your treatment.

This can be a Fixed rate or an amount announced by a specialist.

rong>Dépassement d'honorairesrong> :

Amount charged by a Doctor for time spent treating a patient.

A Doctor in "Secteur 1" will NOT charge over the"Tarif de Convention" and you will be totally reimbursed even on the lowest levels of Top-UP.

A Doctor in "Secteur 2" can charge over the "Tarif de Convention" and you will only be reimbursed if you have a higher level of "Top-Up".

You could be faced with "Dépassement d'honoraires" for a simple 15 minute Specialist visit or for 4 hours of Major Surgery.

Rates charged must be communicated in advance, get in contact with the administration if not. .

rong>Tarif de Conventionrong> :

Base rate given to medical treatment recognizable by a code that indicates its nature and tariff called “Nomenclature” fixed by the “CCAM”(Classification Commune des Actes Médicaux).

The “Tarif de Convention” fixes the 100% base rate that all medical professionals use but it does NOT limit their fees charged.

Top-Ups relate to the base rate and NOT to actual expenses. .

rong>Ticket modérateurrong> :

This represents the difference between your “Régime Obligatoire” reimbursements and the "Tarif de Convention".

This amount, normally reimbursed by a Top-Up will be reimbursed by your “Régime Obligatoire” in case of long-term illness, handicap or maternity.

The “100%” or the "TM" referred to on "Tiers Payant“ slips from Top-Ups will guarantee payment of the "Ticket Moderateur" to any professional accepting to use this facility without having to advance any money. .

rong>Part Régime Obligaroirerong> :

The Percentage of the "Tarif de Convention" that is covered by your “Régime Obligatoire”.

Usually these reimbursements come from "CPAM" or “RSI” if you are self employed.

Reimbursements range from 35% to 100% but are commonly referred to as 70% of the "Tarif de Convention".

Once fully into the French system you will receive a “Carte Vitale”.

This card replaces payment to medical professionals equipped with the “System Noemi”.

rong>Part Régime Complémentairerong> :

"Part Mutuelle". This is the amount paid on your behalf by a Top-Up.

"Dépassement d'honoraires" can be reimbursed by a Top-Up.

Top-Ups starts at 100% and can go up to 600% or more depending on your needs and especially what area you live in.

SOFICA’s sugests middle cover, around 200% for hospitalization permitting you to use Doctors charging twice the "Tarif de Convention“ but lower for the rest as some base rates are very low.

rong>Hors Nomenclaturerong>:

These are treatments that are NOT included on the “CCAM” list thus they do not have a base rate.

These treatments are often in addition to ongoing treatment.

The “CCAM” tend to exclude preventative medicines, "Médecines douces“ that have not been accepted by the “Académie des Sciences”.

Some Top-Ups reimburse thing like osteopathy and homeopathy using Fixed rates set by the companies called “Forfait Annuel”.

rong>

rong>

rong>

Examples of reimbursement: rong>

rong> rong>

rong>rong>

rong> SOFICAS clients benifit fully from the French system as we use French companies that know thier subject.rong>

rong>rong>

"Télétransmition"

Automatic reimbursements using only your "Carte Vitale".

rong>rong>

"Tiers Payant"

No money to be advanced at the chemist / lab / x-ray and more.

rong>rong>

"Prise en charge"

Possible on demand even for Optical and Dentistry.

rong>rong>

Hospitals stay expenses can be paid directly by your "Top-Up".

"Frais de séjours and chambre particulière"

rong>

rong>

rong>rong>

rong>

Hospitalization / Hospitalisation:rong>

rong>rong>

rong>rong>

rong>The question of payment will come after your wellbeing

If you are in an emergency situation, you will be taken care of regardless of your nationality, professional or financial situation.

However, after this point or if you have a planned hospital stay you could be asked for a “PEC”.

This "PEC" enables the hospital or Clinique to claim amounts due for your treatments directly from your "Régime Obligatoire" and eventually your "TOP-UP".rong>

rong>rong>

rong>If you are in France on holiday you may present your “EHIC”.

You will be asked for your blood group card - "carte de groupe sanguin'".

They will ask about allergies - "avez-vous des allergies?" or "êtes-vous allergique?".

You will be asked for your medrong>rong style="color: #000000;">icarong>rong style="color: #000000;">l hirong>rong style="color: #000000;">story rong>rong style="color: #000000;">- "rong>rong style="color: red;">antécédents médicaux ou chirurgicrong>rong style="color: red;">auxrong>rong>".

rong>rong> You will be asked about any medication you are taking – "rong>rong style="color: #ff0000;">Quel est votre traitement actuel / courant/ en cours?rong>rong>"

rong>rong> They will ask about your diet – "rong>rong style="color: #ff0000;">Avez-vous un régime spécial?rong>rong>" Without salt – "rong>rong style="color: #ff0000;">Sans selrong>rong>" Without sugar – "rong>rong style="color: #ff0000;">Sans sucrerong>rong>" Gluten free – "rong>rong style="color: #ff0000;">Sans glutenrong>rong>"rong>

rong>rong>

rong>Key Words:rong>

|

rong>rong>

rong>rong>

rong>Useful Phrases:rong>

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Aching |

Douloureux |

| Ambulance |

Ambulance |

| Anaesthetic |

Anesthésique |

| Anaesthetic |

Anesthésie |

| Ankle |

La cheville |

| Appendix |

L'appendice |

| Arm |

Le bras |

| Assistant nurse |

Aide soignante |

| Back |

Le dos |

| Back of the neck |

La nuque |

| Bedpan |

Un bassin |

| Bell / buzzer |

Sonnette |

| Bladder |

La vessie |

| Blood |

Le sang |

| Blood test |

Prise de sang |

| Blood test (results) |

Résultat sanguin, Bilan sanguin |

| Blood test to be taken fasting |

Prise de sang à jeun |

| Body |

Le corps |

| Bone |

L'os |

| Bottle |

Une bouteille |

| Bowels |

Les intestins |

| Brain |

Le cerveau |

| Breast |

Le sein |

| Bruise |

Un bleu /une contusion / un hématome |

| Burn |

une brûlure |

| Burning sensation |

Sensation de chaleur / douleur cuisante |

| Buttocks / bottom |

Les fesses |

| Calf |

Le mollet |

| Capsule |

Gélule |

| Car accident |

Accident de la route |

| Casualty / A&E |

Urgences |

| Change your dressing |

Faire votre pansement |

| Cheeks |

Les joues |

| Chest |

La poitrine |

| Chin |

Le menton |

| Collarbone |

La clavicule |

| Contraceptive pill |

La pilule |

| Cough / a cough |

Tousser / une toux |

| Covered in bruised |

Etre couvert de bleus |

| Crushed |

Ecrasé / broyé |

| Crutches |

Les béquilles |

| Cut |

coupe |

| Dizziness |

le vertige |

| Doctor |

Médecin |

| Drawsheet |

L’alèse |

| Dressing gown |

robe de chambre |

| Drink (A) |

Une boisson |

| Drink (To) |

Boire |

| Ear |

L'oreille |

| Eat |

Manger |

| ECG |

Electrocardiogramme (électro) |

| Elbow |

Le coude |

| Exhausted |

épuisé |

| Eye (eyes) |

L’œil (Les yeux) |

| Face |

Le visage |

| Face flannel |

Un gant de toilette |

| Feel sick |

J'ai des nausées / J'ai mal au cœur |

| Feel unwell / faint |

J'ai un malaise / j'ai la tête qui tourne |

| Finger |

Le doigt |

| Fingernail |

L'ongle |

| Foot |

Le pied |

| Forehead |

Le front |

| Gall bladder |

La vésicule biliaire |

| Get undressed |

Déshabillez-vous |

| Grazed |

écorché |

| Gum |

Gencive |

| Hand |

La main |

| Have a wash |

Faire sa toilette |

| Head |

La tête |

| Heart |

Le cœur |

| Heel |

Le talon |

| High temperature |

la fièvre |

| Hip |

La hanche |

| Hospital gown (open at the back) |

Casaque / blouse opératoire |

| Infection |

Infection |

| Injection |

Piqûre |

| Intensive care |

Soins intensive |

| Jaw |

La mâchoire |

| Kidney |

Le rein |

| Knee |

Le genou |

| Liver |

Le foie |

| Lower back |

Les lombaires / les reins |

| Lungs |

Les poumons |

| Make the bed |

Faire le lit |

| Meal |

Un repas |

| Medicine (treatment) |

Médicament / traitement |

| Mouth |

La bouche |

| Muscle |

Le muscle |

| Nausea |

la nausée |

| Neck |

Le cou |

| Nightdress |

Chemise de nuit |

| Nose |

Le nez |

| Nurse |

Infirmière |

| Operating theatre |

Bloc opératoire |

| Operation |

Intervention chirurgicale |

| Operation |

Intervention |

| Out of breath |

essoufflé |

| Pain killer |

Calmant |

| Paramedics |

SAMU |

| Permission to operate |

Autorisation d’opérer |

| Physio after an accident |

Re-éducation |

| Physiotherapist |

Kinésithérapeute |

| Physiotherapy |

Kinésithérapie |

| Pill |

Cachet / Comprime |

| Pyjamas |

Pyjama |

| Rib |

La côte |

| Scratch |

une égratignure |

| Sensitive |

Sensible |

| Set up a drip |

Faire une perfusion |

| Shoulder |

L’épaule |

| Sleeping pill |

Somnifère |

| Slippers |

Pantoufles |

| Soap |

Le savon |

| Sore |

endolori |

| Spleen |

La rate |

| Sticking plaster |

Sparadrap / pansement adhésif |

| Stitches |

Points de suture |

| Stomach (external) |

Le ventre |

| Stomach (internal) |

L'estomac |

| Stretcher |

Brancard |

| Surgeon |

Chirurgien |

| Surgical dressing |

Pansement |

| Swelling |

une bosse |

| Swollen |

enfle |

| Take your blood pressure |

Contrôler votre tension |

| Teeth |

Les dents |

| Tender |

sensible |

| Tendon |

Le tendon |

| Thigh |

La cuisse |

| Throat |

La gorge |

| Thumb |

Le pouce |

| Tired |

fatigue |

| Toenail |

L'ongle du pied |

| Toes |

Les orteils |

| Tongue |

Le langue |

| Towel |

Une serviette |

| Ulcer |

ulcère |

| Water |

L'eau |

| Wheelchair |

Fauteuil roulant |

| Wounded |

blessé |

| Wrist |

Le poignet |

| X-ray |

Radio |

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Call an ambulance |

Appeler une ambulance |

| Call the emergency services |

Appeler le urgences |

| Call the police |

Appeler la police |

| Do not get up |

Ne pas se lever |

| Do you know an English speeking doctor? |

Connaissez-vous un médecin qui parle anglais? |

| Do you want an injection? |

Voulez-vous une piqûre? |

| I am allergic to… |

Je suis allergique a / a la / aux… |

| I am constipated |

Je suis constipé(e) |

| I am diabetic |

J'ai le diabète |

| I am going to faint |

Je vais m’evanouir |

| I am in pain |

J'ai mal |

| I am taking medication |

Je prends des médicament |

| I don't feel very well |

Je ne me sens pas tres bien |

| I feel better |

Je me sens mieux |

| I feel sick |

J'ai envie de vomir / J'ai mal au cœur |

| I feel bad |

Je me sens mal |

| I feel weak |

Je me sent faible |

| I feel worse |

Je me sens moins bien |

| I fell over |

Je suis tomber |

| I have a broken bone |

J’ai une fracture |

| I have a broken tooth |

J'ai une dent cassée |

| I have a chest cold |

J’ai une bronchite |

| I have a cold |

Je suis enrhumé |

| I have a cold |

J’ai une rhume |

| I have a got fever |

J’ai de la fievre |

| I have a headache |

J'ai mal à la tête |

| I have a sore throat / tonsilitis |

J'ai mal a la gorge / j'ai une angine |

| I have a wound |

J’ai une blessure |

| I have an abscess |

J'ai un abcès |

| I have an abscess |

J’ai un abcès |

| I have back ache |

J'ai mal au dos |

| I have been sick |

J'ai vomi |

| I have burnt myself |

Je me suis brûlé |

| I have chest pains |

J’ai des douleur à la poitrine |

| I have cut myself |

Je me suis coupé |

| I have flu |

J'ai la grippe |

| I have gor a head ache |

J’ai mal à la tête |

| I have got a headache |

J’ai mal à la tête |

| I have got a sore throat |

J’ai mal à la gorge |

| I have got a stomach ache |

J’ai mal à l’estomac |

| I have got cramps |

J’ai des cramps |

| I have got diarrhea |

J’ai la diarrhea |

| I have had a heart attack |

J’ai eu une crise cardiaque |

| I have lost a filling |

J'ai perdu un plombage |

| I have pain |

J'ai de la douleur |

| I have pains in the chest |

J'ai mal à la poitrine |

| I have shivers |

J’ai des frissons |

| I have stomach ache |

J'ai mal au ventre |

| I have the flu |

J’ai la grippe |

| I have to see a doctor |

J'ai dois de voir un médecin |

| I have toothache |

J'ai mal aux dents |

| I have wind |

J'ai des gaz |

| I need a bedpan |

J’ai besoin d'un bassin |

| I think it's broken |

Je pense que c'est cassé |

| I want a pee |

Je veux faire pipi |

| I'm bleeding |

Je saigne |

| I'm dizzy |

J’ai la vertige |

| I'm hungry |

J'ai faim |

| I'm sick |

Je suis malade |

| I'm sweating |

Je transpire |

| I'm thirsty |

J'ai soif |

| Is it serious? |

C’est grave? |

| It hurts everywhere |

J’ai mal partôut |

| It hurts here |

J’ai mal ici |

| It is painful since… |

C'est douloureux depuis… |

| Its swelling |

Ca enfle |

| I've been sick |

J'ai vomi |

| I've got the shivers |

J'ai des frissons |

| Permanent filling |

Obturation définitive |

| Stay lying down |

Restez allongé |

| Temporary filling |

Obturation provisoire |

| That hurts |

ça me fait Mal |

| That hurts! |

Ca me fait mal ! |

| That is very painful |

C'est très douloureux |

| That itches |

Ca me démange |

| That itches |

Ca me gratte |

| That tickles |

Ca me chatouille |

| That's too loose |

Ce n'est pas assez serré |

| That's too tight |

C'est trop serré |

| There has been an accident |

Il y a eu un accident |

| To have a bowel movement (phoo) |

Aller à la selle (faire caca) |

| To ring (for a nurse) |

Sonner l'infermiere |

| To urinate |

Uriner (faire pipi) |

| Where is the Chemist? |

Ou se trouve la pharmacie? |

| Where is the Doctors? |

Ou se trouve un medecin? |

| Where is the Hospital? |

Ou se trouve l'hôpital? |

|

Partners

Health cover in France - How does it work ?

-

rong>HOW DOES IT WORKrong>

rong style="font-size: 14pt;"> rong>

rong style="font-size: 14pt;"> rong>

rong style="font-size: 14pt;">rong>

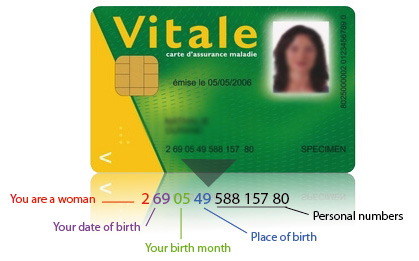

Know your number off by heart !

In the event that you are taken ill without you personal

belongings, just by telling you "numéro de Sécurité Sociale"

the medical services will have enough information to get started.

The first number designates your sex, 1 for men and 2 for women.

For temporary numbers starting with 5, 6, 7 or 8 this logic does not apply.

The next four numbers indicate your year and month of birth.

Your "insee" number will probably be followed by 99 for foreigners.

This number is replaced by the department code if you were born in France.

e.g.: 24 if you were born in the Dordogne.

Finally, a series of 8 numbers show what “CPAM” office treats your dossiers.

"How to use your "Carte Vitale" & "Top-Up"

When you have medical treatment in France, you are usually asked for your “CARTE VITALE” (from CPAM or RSI) and the slip of paper called “Tiers payant complémentaire or Mutuelle" (from your Top-Up). Usually no money is asked for. The bill will be sent to “CPAM” (Caisse Primaire d’Assurance Maladie or other if selfemployed) and your TOP-UP.

When only your Carte Vitale is asked for this is usually because there is the possibility of using the “Télétransmission” (automatic payment and reimbursement system). You will have to pay either the total amount (eg: GP, Dentist) or just the “Ticket Modérateur” difference between the CPAM allowance and the “Tarif de convention” (100%

base rate (what the state says your treatment is worth).

CPAM will proceed with their partial reimbursement and send the information(normally) to your Top-Up by Télétransmission.

Your Top-Up will in turn reimburse the difference depending on your chosen level of cover.

In some cases you will have to pay for excess charges that the “Médecin Spécialiste” has over the state convention rate. These are called in French “Dépassements d’honoraires”.

These charges can be claimed from your Top-up by sending the an acquitted bill. (! If your level of guarantee covers such charges).

If the CPAM does not reimburse medical treatment then the Top-up will not either, unless otherwise stated by annual flat rate.

(eg: Private room, glasses, spa, flu injection, etc.)

How to use "Feuille de Soins" or "Factures"

When your “Carte Vitale” is not used, papers called “FEUILLES DE SOINS” are given to you.

The information on these papers is identical to the information given by your “Carte Vitale”.

These forms have to be filled in and sent to the CPAM office dealing with your reimbursements.

! Please make sure you fill in your Social Security number (also called numéro d’immatriculation) and sign the paperwork at the bottom.

If for whatever reason the Top-up takes time reimbursing their part on reception of the CPAM statement itemising your last reimbursements, send these to your Top-up.

(This replaces the Télétransmission should CPAM not have sent the information in the first place).

As soon as your Top-up has the correct information they too can reimburse their part.

N.B: If you send your paperwork directly to your insurance company, then the reimbursements will be a lot quicker than if you send them to your brokers, “SOFICA’s”. Please, do not forget to indicate your contract number.

Partners

Health cover in France - A few definitions

rong>A FEW DEFINITIONSrong>

rong>

rong>

rong>

rong>

rong>

rong>

rong>

Understanding The French System:

rong>

rong>rong>

Unlike the English system, the French regime makes no difference between the public and private treatments

(the reimbursement rates are identical).

On the other-hand, the 'Sécurité Sociale' alone does not cover the entirety of your expenses.

rong style="text-align: center;">

rong style="text-align: center;">rong style="text-align: center;">First column represents the total cost of your medical treatment. rong>

rong>

rong style="text-align: center;">rong style="text-align: center;">

rong style="text-align: center;">Second column shows the possible reimbursements:

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange = reimbursable with minimum cover

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange to Red = Only reimbursable with higher cover or not at all.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Third column indicates where the reimbursements could come from.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Click on each column to see their individual definitions:

rong>

rong style="text-align: center;">rong>

rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>

rong>Frais Médicauxrong> :

The TOTAL amount charged for your treatment.

This can be a Fixed rate or an amount announced by a specialist.

rong>Dépassement d'honorairesrong> :

Amount charged by a Doctor for time spent treating a patient.

A Doctor in "Secteur 1" will NOT charge over the"Tarif de Convention" and you will be totally reimbursed even on the lowest levels of Top-UP.

A Doctor in "Secteur 2" can charge over the "Tarif de Convention" and you will only be reimbursed if you have a higher level of "Top-Up".

You could be faced with "Dépassement d'honoraires" for a simple 15 minute Specialist visit or for 4 hours of Major Surgery.

Rates charged must be communicated in advance, get in contact with the administration if not. .

rong>Tarif de Conventionrong> :

Base rate given to medical treatment recognizable by a code that indicates its nature and tariff called “Nomenclature” fixed by the “CCAM”(Classification Commune des Actes Médicaux).

The “Tarif de Convention” fixes the 100% base rate that all medical professionals use but it does NOT limit their fees charged.

Top-Ups relate to the base rate and NOT to actual expenses. .

rong>Ticket modérateurrong> :

This represents the difference between your “Régime Obligatoire” reimbursements and the "Tarif de Convention".

This amount, normally reimbursed by a Top-Up will be reimbursed by your “Régime Obligatoire” in case of long-term illness, handicap or maternity.

The “100%” or the "TM" referred to on "Tiers Payant“ slips from Top-Ups will guarantee payment of the "Ticket Moderateur" to any professional accepting to use this facility without having to advance any money. .

rong>Part Régime Obligaroirerong> :

The Percentage of the "Tarif de Convention" that is covered by your “Régime Obligatoire”.

Usually these reimbursements come from "CPAM" or “RSI” if you are self employed.

Reimbursements range from 35% to 100% but are commonly referred to as 70% of the "Tarif de Convention".

Once fully into the French system you will receive a “Carte Vitale”.

This card replaces payment to medical professionals equipped with the “System Noemi”.

rong>Part Régime Complémentairerong> :

"Part Mutuelle". This is the amount paid on your behalf by a Top-Up.

"Dépassement d'honoraires" can be reimbursed by a Top-Up.

Top-Ups starts at 100% and can go up to 600% or more depending on your needs and especially what area you live in.

SOFICA’s sugests middle cover, around 200% for hospitalization permitting you to use Doctors charging twice the "Tarif de Convention“ but lower for the rest as some base rates are very low.

rong>Hors Nomenclaturerong>:

These are treatments that are NOT included on the “CCAM” list thus they do not have a base rate.

These treatments are often in addition to ongoing treatment.

The “CCAM” tend to exclude preventative medicines, "Médecines douces“ that have not been accepted by the “Académie des Sciences”.

Some Top-Ups reimburse thing like osteopathy and homeopathy using Fixed rates set by the companies called “Forfait Annuel”.

rong>

rong>

rong>

Examples of reimbursement: rong>

rong> rong>

rong>rong>

rong> SOFICAS clients benifit fully from the French system as we use French companies that know thier subject.rong>

rong>rong>

"Télétransmition"

Automatic reimbursements using only your "Carte Vitale".

rong>rong>

"Tiers Payant"

No money to be advanced at the chemist / lab / x-ray and more.

rong>rong>

"Prise en charge"

Possible on demand even for Optical and Dentistry.

rong>rong>

Hospitals stay expenses can be paid directly by your "Top-Up".

"Frais de séjours and chambre particulière"

rong>

rong>

rong>rong>

rong>

Hospitalization / Hospitalisation:rong>

rong>rong>

rong>rong>

rong>The question of payment will come after your wellbeing

If you are in an emergency situation, you will be taken care of regardless of your nationality, professional or financial situation.

However, after this point or if you have a planned hospital stay you could be asked for a “PEC”.

This "PEC" enables the hospital or Clinique to claim amounts due for your treatments directly from your "Régime Obligatoire" and eventually your "TOP-UP".rong>

rong>rong>

rong>If you are in France on holiday you may present your “EHIC”.

You will be asked for your blood group card - "carte de groupe sanguin'".

They will ask about allergies - "avez-vous des allergies?" or "êtes-vous allergique?".

You will be asked for your medrong>rong style="color: #000000;">icarong>rong style="color: #000000;">l hirong>rong style="color: #000000;">story rong>rong style="color: #000000;">- "rong>rong style="color: red;">antécédents médicaux ou chirurgicrong>rong style="color: red;">auxrong>rong>".

rong>rong> You will be asked about any medication you are taking – "rong>rong style="color: #ff0000;">Quel est votre traitement actuel / courant/ en cours?rong>rong>"

rong>rong> They will ask about your diet – "rong>rong style="color: #ff0000;">Avez-vous un régime spécial?rong>rong>" Without salt – "rong>rong style="color: #ff0000;">Sans selrong>rong>" Without sugar – "rong>rong style="color: #ff0000;">Sans sucrerong>rong>" Gluten free – "rong>rong style="color: #ff0000;">Sans glutenrong>rong>"rong>

rong>rong>

rong>Key Words:rong>

|

rong>rong>

rong>rong>

rong>Useful Phrases:rong>

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Aching |

Douloureux |

| Ambulance |

Ambulance |

| Anaesthetic |

Anesthésique |

| Anaesthetic |

Anesthésie |

| Ankle |

La cheville |

| Appendix |

L'appendice |

| Arm |

Le bras |

| Assistant nurse |

Aide soignante |

| Back |

Le dos |

| Back of the neck |

La nuque |

| Bedpan |

Un bassin |

| Bell / buzzer |

Sonnette |

| Bladder |

La vessie |

| Blood |

Le sang |

| Blood test |

Prise de sang |

| Blood test (results) |

Résultat sanguin, Bilan sanguin |

| Blood test to be taken fasting |

Prise de sang à jeun |

| Body |

Le corps |

| Bone |

L'os |

| Bottle |

Une bouteille |

| Bowels |

Les intestins |

| Brain |

Le cerveau |

| Breast |

Le sein |

| Bruise |

Un bleu /une contusion / un hématome |

| Burn |

une brûlure |

| Burning sensation |

Sensation de chaleur / douleur cuisante |

| Buttocks / bottom |

Les fesses |

| Calf |

Le mollet |

| Capsule |

Gélule |

| Car accident |

Accident de la route |

| Casualty / A&E |

Urgences |

| Change your dressing |

Faire votre pansement |

| Cheeks |

Les joues |

| Chest |

La poitrine |

| Chin |

Le menton |

| Collarbone |

La clavicule |

| Contraceptive pill |

La pilule |

| Cough / a cough |

Tousser / une toux |

| Covered in bruised |

Etre couvert de bleus |

| Crushed |

Ecrasé / broyé |

| Crutches |

Les béquilles |

| Cut |

coupe |

| Dizziness |

le vertige |

| Doctor |

Médecin |

| Drawsheet |

L’alèse |

| Dressing gown |

robe de chambre |

| Drink (A) |

Une boisson |

| Drink (To) |

Boire |

| Ear |

L'oreille |

| Eat |

Manger |

| ECG |

Electrocardiogramme (électro) |

| Elbow |

Le coude |

| Exhausted |

épuisé |

| Eye (eyes) |

L’œil (Les yeux) |

| Face |

Le visage |

| Face flannel |

Un gant de toilette |

| Feel sick |

J'ai des nausées / J'ai mal au cœur |

| Feel unwell / faint |

J'ai un malaise / j'ai la tête qui tourne |

| Finger |

Le doigt |

| Fingernail |

L'ongle |

| Foot |

Le pied |

| Forehead |

Le front |

| Gall bladder |

La vésicule biliaire |

| Get undressed |

Déshabillez-vous |

| Grazed |

écorché |

| Gum |

Gencive |

| Hand |

La main |

| Have a wash |

Faire sa toilette |

| Head |

La tête |

| Heart |

Le cœur |

| Heel |

Le talon |

| High temperature |

la fièvre |

| Hip |

La hanche |

| Hospital gown (open at the back) |

Casaque / blouse opératoire |

| Infection |

Infection |

| Injection |

Piqûre |

| Intensive care |

Soins intensive |

| Jaw |

La mâchoire |

| Kidney |

Le rein |

| Knee |

Le genou |

| Liver |

Le foie |

| Lower back |

Les lombaires / les reins |

| Lungs |

Les poumons |

| Make the bed |

Faire le lit |

| Meal |

Un repas |

| Medicine (treatment) |

Médicament / traitement |

| Mouth |

La bouche |

| Muscle |

Le muscle |

| Nausea |

la nausée |

| Neck |

Le cou |

| Nightdress |

Chemise de nuit |

| Nose |

Le nez |

| Nurse |

Infirmière |

| Operating theatre |

Bloc opératoire |

| Operation |

Intervention chirurgicale |

| Operation |

Intervention |

| Out of breath |

essoufflé |

| Pain killer |

Calmant |

| Paramedics |

SAMU |

| Permission to operate |

Autorisation d’opérer |

| Physio after an accident |

Re-éducation |

| Physiotherapist |

Kinésithérapeute |

| Physiotherapy |

Kinésithérapie |

| Pill |

Cachet / Comprime |

| Pyjamas |

Pyjama |

| Rib |

La côte |

| Scratch |

une égratignure |

| Sensitive |

Sensible |

| Set up a drip |

Faire une perfusion |

| Shoulder |

L’épaule |

| Sleeping pill |

Somnifère |

| Slippers |

Pantoufles |

| Soap |

Le savon |

| Sore |

endolori |

| Spleen |

La rate |

| Sticking plaster |

Sparadrap / pansement adhésif |

| Stitches |

Points de suture |

| Stomach (external) |

Le ventre |

| Stomach (internal) |

L'estomac |

| Stretcher |

Brancard |

| Surgeon |

Chirurgien |

| Surgical dressing |

Pansement |

| Swelling |

une bosse |

| Swollen |

enfle |

| Take your blood pressure |

Contrôler votre tension |

| Teeth |

Les dents |

| Tender |

sensible |

| Tendon |

Le tendon |

| Thigh |

La cuisse |

| Throat |

La gorge |

| Thumb |

Le pouce |

| Tired |

fatigue |

| Toenail |

L'ongle du pied |

| Toes |

Les orteils |

| Tongue |

Le langue |

| Towel |

Une serviette |

| Ulcer |

ulcère |

| Water |

L'eau |

| Wheelchair |

Fauteuil roulant |

| Wounded |

blessé |

| Wrist |

Le poignet |

| X-ray |

Radio |

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Call an ambulance |

Appeler une ambulance |

| Call the emergency services |

Appeler le urgences |

| Call the police |

Appeler la police |

| Do not get up |

Ne pas se lever |

| Do you know an English speeking doctor? |

Connaissez-vous un médecin qui parle anglais? |

| Do you want an injection? |

Voulez-vous une piqûre? |

| I am allergic to… |

Je suis allergique a / a la / aux… |

| I am constipated |

Je suis constipé(e) |

| I am diabetic |

J'ai le diabète |

| I am going to faint |

Je vais m’evanouir |

| I am in pain |

J'ai mal |

| I am taking medication |

Je prends des médicament |

| I don't feel very well |

Je ne me sens pas tres bien |

| I feel better |

Je me sens mieux |

| I feel sick |

J'ai envie de vomir / J'ai mal au cœur |

| I feel bad |

Je me sens mal |

| I feel weak |

Je me sent faible |

| I feel worse |

Je me sens moins bien |

| I fell over |

Je suis tomber |

| I have a broken bone |

J’ai une fracture |

| I have a broken tooth |

J'ai une dent cassée |

| I have a chest cold |

J’ai une bronchite |

| I have a cold |

Je suis enrhumé |

| I have a cold |

J’ai une rhume |

| I have a got fever |

J’ai de la fievre |

| I have a headache |

J'ai mal à la tête |

| I have a sore throat / tonsilitis |

J'ai mal a la gorge / j'ai une angine |

| I have a wound |

J’ai une blessure |

| I have an abscess |

J'ai un abcès |

| I have an abscess |

J’ai un abcès |

| I have back ache |

J'ai mal au dos |

| I have been sick |

J'ai vomi |

| I have burnt myself |

Je me suis brûlé |

| I have chest pains |

J’ai des douleur à la poitrine |

| I have cut myself |

Je me suis coupé |

| I have flu |

J'ai la grippe |

| I have gor a head ache |

J’ai mal à la tête |

| I have got a headache |

J’ai mal à la tête |

| I have got a sore throat |

J’ai mal à la gorge |

| I have got a stomach ache |

J’ai mal à l’estomac |

| I have got cramps |

J’ai des cramps |

| I have got diarrhea |

J’ai la diarrhea |

| I have had a heart attack |

J’ai eu une crise cardiaque |

| I have lost a filling |

J'ai perdu un plombage |

| I have pain |

J'ai de la douleur |

| I have pains in the chest |

J'ai mal à la poitrine |

| I have shivers |

J’ai des frissons |

| I have stomach ache |

J'ai mal au ventre |

| I have the flu |

J’ai la grippe |

| I have to see a doctor |

J'ai dois de voir un médecin |

| I have toothache |

J'ai mal aux dents |

| I have wind |

J'ai des gaz |

| I need a bedpan |

J’ai besoin d'un bassin |

| I think it's broken |

Je pense que c'est cassé |

| I want a pee |

Je veux faire pipi |

| I'm bleeding |

Je saigne |

| I'm dizzy |

J’ai la vertige |

| I'm hungry |

J'ai faim |

| I'm sick |

Je suis malade |

| I'm sweating |

Je transpire |

| I'm thirsty |

J'ai soif |

| Is it serious? |

C’est grave? |

| It hurts everywhere |

J’ai mal partôut |

| It hurts here |

J’ai mal ici |

| It is painful since… |

C'est douloureux depuis… |

| Its swelling |

Ca enfle |

| I've been sick |

J'ai vomi |

| I've got the shivers |

J'ai des frissons |

| Permanent filling |

Obturation définitive |

| Stay lying down |

Restez allongé |

| Temporary filling |

Obturation provisoire |

| That hurts |

ça me fait Mal |

| That hurts! |

Ca me fait mal ! |

| That is very painful |

C'est très douloureux |

| That itches |

Ca me démange |

| That itches |

Ca me gratte |

| That tickles |

Ca me chatouille |

| That's too loose |

Ce n'est pas assez serré |

| That's too tight |

C'est trop serré |

| There has been an accident |

Il y a eu un accident |

| To have a bowel movement (phoo) |

Aller à la selle (faire caca) |

| To ring (for a nurse) |

Sonner l'infermiere |

| To urinate |

Uriner (faire pipi) |

| Where is the Chemist? |

Ou se trouve la pharmacie? |

| Where is the Doctors? |

Ou se trouve un medecin? |

| Where is the Hospital? |

Ou se trouve l'hôpital? |

|

Partners

Health cover in France - How does it work ?

-

rong>HOW DOES IT WORKrong>

rong style="font-size: 14pt;"> rong>

rong style="font-size: 14pt;"> rong>

rong style="font-size: 14pt;">rong>

Know your number off by heart !

In the event that you are taken ill without you personal

belongings, just by telling you "numéro de Sécurité Sociale"

the medical services will have enough information to get started.

The first number designates your sex, 1 for men and 2 for women.

For temporary numbers starting with 5, 6, 7 or 8 this logic does not apply.

The next four numbers indicate your year and month of birth.

Your "insee" number will probably be followed by 99 for foreigners.

This number is replaced by the department code if you were born in France.

e.g.: 24 if you were born in the Dordogne.

Finally, a series of 8 numbers show what “CPAM” office treats your dossiers.

"How to use your "Carte Vitale" & "Top-Up"

When you have medical treatment in France, you are usually asked for your “CARTE VITALE” (from CPAM or RSI) and the slip of paper called “Tiers payant complémentaire or Mutuelle" (from your Top-Up). Usually no money is asked for. The bill will be sent to “CPAM” (Caisse Primaire d’Assurance Maladie or other if selfemployed) and your TOP-UP.

When only your Carte Vitale is asked for this is usually because there is the possibility of using the “Télétransmission” (automatic payment and reimbursement system). You will have to pay either the total amount (eg: GP, Dentist) or just the “Ticket Modérateur” difference between the CPAM allowance and the “Tarif de convention” (100%

base rate (what the state says your treatment is worth).

CPAM will proceed with their partial reimbursement and send the information(normally) to your Top-Up by Télétransmission.

Your Top-Up will in turn reimburse the difference depending on your chosen level of cover.

In some cases you will have to pay for excess charges that the “Médecin Spécialiste” has over the state convention rate. These are called in French “Dépassements d’honoraires”.

These charges can be claimed from your Top-up by sending the an acquitted bill. (! If your level of guarantee covers such charges).

If the CPAM does not reimburse medical treatment then the Top-up will not either, unless otherwise stated by annual flat rate.

(eg: Private room, glasses, spa, flu injection, etc.)

How to use "Feuille de Soins" or "Factures"

When your “Carte Vitale” is not used, papers called “FEUILLES DE SOINS” are given to you.

The information on these papers is identical to the information given by your “Carte Vitale”.

These forms have to be filled in and sent to the CPAM office dealing with your reimbursements.

! Please make sure you fill in your Social Security number (also called numéro d’immatriculation) and sign the paperwork at the bottom.

If for whatever reason the Top-up takes time reimbursing their part on reception of the CPAM statement itemising your last reimbursements, send these to your Top-up.

(This replaces the Télétransmission should CPAM not have sent the information in the first place).

As soon as your Top-up has the correct information they too can reimburse their part.

N.B: If you send your paperwork directly to your insurance company, then the reimbursements will be a lot quicker than if you send them to your brokers, “SOFICA’s”. Please, do not forget to indicate your contract number.

Partners

Downloads

rong style="color: #006699;">Companyrong>

|

rong style="color: #006699;">Click onrong>

rong>

rong style="color: #006699;">icon to downloadrong>

rong>

|

rong style="color: #006699;">Document name

or descriptionrong>

|

rong style="color: #006699;">Click onrong>

rong>

rong style="color: #006699;">icon to downloadrong>

rong>

|

rong style="color: #006699; font-size: 22px;">Document name

or descriptionrong>

|

rong style="color: #006699;">SOFICASrong>

|

|

rong>rong> |

|

|

|

|

|

|

|

rong>AFPSrong>

rong>GIEPS

rong>

|

|

|

|

|

|

|

|

|

|

rong>

rong>

|

|

|

|

|

| |

|

|

|

|

rong style="color: #185f9c; font-size: 24px;">SERENOVArong>

|

|

|

|

|

| | | | | |

rong>APRILrong>

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Partners

Health cover in France - A few definitions

rong>A FEW DEFINITIONSrong>

rong>

rong>

rong>

rong>

rong>

rong>

rong>

Understanding The French System:

rong>

rong>rong>

Unlike the English system, the French regime makes no difference between the public and private treatments

(the reimbursement rates are identical).

On the other-hand, the 'Sécurité Sociale' alone does not cover the entirety of your expenses.

rong style="text-align: center;">

rong style="text-align: center;">rong style="text-align: center;">First column represents the total cost of your medical treatment. rong>

rong>

rong style="text-align: center;">rong style="text-align: center;">

rong style="text-align: center;">Second column shows the possible reimbursements:

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange = reimbursable with minimum cover

rong>

rong style="text-align: center;">

rong style="text-align: center;">Orange to Red = Only reimbursable with higher cover or not at all.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Third column indicates where the reimbursements could come from.

rong>

rong style="text-align: center;">

rong style="text-align: center;">Click on each column to see their individual definitions:

rong>

rong style="text-align: center;">rong>

rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">rong style="text-align: center;">

rong>rong>rong>rong>rong>rong>rong>

rong>Frais Médicauxrong> :

The TOTAL amount charged for your treatment.

This can be a Fixed rate or an amount announced by a specialist.

rong>Dépassement d'honorairesrong> :

Amount charged by a Doctor for time spent treating a patient.

A Doctor in "Secteur 1" will NOT charge over the"Tarif de Convention" and you will be totally reimbursed even on the lowest levels of Top-UP.

A Doctor in "Secteur 2" can charge over the "Tarif de Convention" and you will only be reimbursed if you have a higher level of "Top-Up".

You could be faced with "Dépassement d'honoraires" for a simple 15 minute Specialist visit or for 4 hours of Major Surgery.

Rates charged must be communicated in advance, get in contact with the administration if not. .

rong>Tarif de Conventionrong> :

Base rate given to medical treatment recognizable by a code that indicates its nature and tariff called “Nomenclature” fixed by the “CCAM”(Classification Commune des Actes Médicaux).

The “Tarif de Convention” fixes the 100% base rate that all medical professionals use but it does NOT limit their fees charged.

Top-Ups relate to the base rate and NOT to actual expenses. .

rong>Ticket modérateurrong> :

This represents the difference between your “Régime Obligatoire” reimbursements and the "Tarif de Convention".

This amount, normally reimbursed by a Top-Up will be reimbursed by your “Régime Obligatoire” in case of long-term illness, handicap or maternity.

The “100%” or the "TM" referred to on "Tiers Payant“ slips from Top-Ups will guarantee payment of the "Ticket Moderateur" to any professional accepting to use this facility without having to advance any money. .

rong>Part Régime Obligaroirerong> :

The Percentage of the "Tarif de Convention" that is covered by your “Régime Obligatoire”.

Usually these reimbursements come from "CPAM" or “RSI” if you are self employed.

Reimbursements range from 35% to 100% but are commonly referred to as 70% of the "Tarif de Convention".

Once fully into the French system you will receive a “Carte Vitale”.

This card replaces payment to medical professionals equipped with the “System Noemi”.

rong>Part Régime Complémentairerong> :

"Part Mutuelle". This is the amount paid on your behalf by a Top-Up.

"Dépassement d'honoraires" can be reimbursed by a Top-Up.

Top-Ups starts at 100% and can go up to 600% or more depending on your needs and especially what area you live in.

SOFICA’s sugests middle cover, around 200% for hospitalization permitting you to use Doctors charging twice the "Tarif de Convention“ but lower for the rest as some base rates are very low.

rong>Hors Nomenclaturerong>:

These are treatments that are NOT included on the “CCAM” list thus they do not have a base rate.

These treatments are often in addition to ongoing treatment.

The “CCAM” tend to exclude preventative medicines, "Médecines douces“ that have not been accepted by the “Académie des Sciences”.

Some Top-Ups reimburse thing like osteopathy and homeopathy using Fixed rates set by the companies called “Forfait Annuel”.

rong>

rong>

rong>

Examples of reimbursement: rong>

rong> rong>

rong>rong>

rong> SOFICAS clients benifit fully from the French system as we use French companies that know thier subject.rong>

rong>rong>

"Télétransmition"

Automatic reimbursements using only your "Carte Vitale".

rong>rong>

"Tiers Payant"

No money to be advanced at the chemist / lab / x-ray and more.

rong>rong>

"Prise en charge"

Possible on demand even for Optical and Dentistry.

rong>rong>

Hospitals stay expenses can be paid directly by your "Top-Up".

"Frais de séjours and chambre particulière"

rong>

rong>

rong>rong>

rong>

Hospitalization / Hospitalisation:rong>

rong>rong>

rong>rong>

rong>The question of payment will come after your wellbeing

If you are in an emergency situation, you will be taken care of regardless of your nationality, professional or financial situation.

However, after this point or if you have a planned hospital stay you could be asked for a “PEC”.

This "PEC" enables the hospital or Clinique to claim amounts due for your treatments directly from your "Régime Obligatoire" and eventually your "TOP-UP".rong>

rong>rong>

rong>If you are in France on holiday you may present your “EHIC”.

You will be asked for your blood group card - "carte de groupe sanguin'".

They will ask about allergies - "avez-vous des allergies?" or "êtes-vous allergique?".

You will be asked for your medrong>rong style="color: #000000;">icarong>rong style="color: #000000;">l hirong>rong style="color: #000000;">story rong>rong style="color: #000000;">- "rong>rong style="color: red;">antécédents médicaux ou chirurgicrong>rong style="color: red;">auxrong>rong>".

rong>rong> You will be asked about any medication you are taking – "rong>rong style="color: #ff0000;">Quel est votre traitement actuel / courant/ en cours?rong>rong>"

rong>rong> They will ask about your diet – "rong>rong style="color: #ff0000;">Avez-vous un régime spécial?rong>rong>" Without salt – "rong>rong style="color: #ff0000;">Sans selrong>rong>" Without sugar – "rong>rong style="color: #ff0000;">Sans sucrerong>rong>" Gluten free – "rong>rong style="color: #ff0000;">Sans glutenrong>rong>"rong>

rong>rong>

rong>Key Words:rong>

|

rong>rong>

rong>rong>

rong>Useful Phrases:rong>

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Aching |

Douloureux |

| Ambulance |

Ambulance |

| Anaesthetic |

Anesthésique |

| Anaesthetic |

Anesthésie |

| Ankle |

La cheville |

| Appendix |

L'appendice |

| Arm |

Le bras |

| Assistant nurse |

Aide soignante |

| Back |

Le dos |

| Back of the neck |

La nuque |

| Bedpan |

Un bassin |

| Bell / buzzer |

Sonnette |

| Bladder |

La vessie |

| Blood |

Le sang |

| Blood test |

Prise de sang |

| Blood test (results) |

Résultat sanguin, Bilan sanguin |

| Blood test to be taken fasting |

Prise de sang à jeun |

| Body |

Le corps |

| Bone |

L'os |

| Bottle |

Une bouteille |

| Bowels |

Les intestins |

| Brain |

Le cerveau |

| Breast |

Le sein |

| Bruise |

Un bleu /une contusion / un hématome |

| Burn |

une brûlure |

| Burning sensation |

Sensation de chaleur / douleur cuisante |

| Buttocks / bottom |

Les fesses |

| Calf |

Le mollet |

| Capsule |

Gélule |

| Car accident |

Accident de la route |

| Casualty / A&E |

Urgences |

| Change your dressing |

Faire votre pansement |

| Cheeks |

Les joues |

| Chest |

La poitrine |

| Chin |

Le menton |

| Collarbone |

La clavicule |

| Contraceptive pill |

La pilule |

| Cough / a cough |

Tousser / une toux |

| Covered in bruised |

Etre couvert de bleus |

| Crushed |

Ecrasé / broyé |

| Crutches |

Les béquilles |

| Cut |

coupe |

| Dizziness |

le vertige |

| Doctor |

Médecin |

| Drawsheet |

L’alèse |

| Dressing gown |

robe de chambre |

| Drink (A) |

Une boisson |

| Drink (To) |

Boire |

| Ear |

L'oreille |

| Eat |

Manger |

| ECG |

Electrocardiogramme (électro) |

| Elbow |

Le coude |

| Exhausted |

épuisé |

| Eye (eyes) |

L’œil (Les yeux) |

| Face |

Le visage |

| Face flannel |

Un gant de toilette |

| Feel sick |

J'ai des nausées / J'ai mal au cœur |

| Feel unwell / faint |

J'ai un malaise / j'ai la tête qui tourne |

| Finger |

Le doigt |

| Fingernail |

L'ongle |

| Foot |

Le pied |

| Forehead |

Le front |

| Gall bladder |

La vésicule biliaire |

| Get undressed |

Déshabillez-vous |

| Grazed |

écorché |

| Gum |

Gencive |

| Hand |

La main |

| Have a wash |

Faire sa toilette |

| Head |

La tête |

| Heart |

Le cœur |

| Heel |

Le talon |

| High temperature |

la fièvre |

| Hip |

La hanche |

| Hospital gown (open at the back) |

Casaque / blouse opératoire |

| Infection |

Infection |

| Injection |

Piqûre |

| Intensive care |

Soins intensive |

| Jaw |

La mâchoire |

| Kidney |

Le rein |

| Knee |

Le genou |

| Liver |

Le foie |

| Lower back |

Les lombaires / les reins |

| Lungs |

Les poumons |

| Make the bed |

Faire le lit |

| Meal |

Un repas |

| Medicine (treatment) |

Médicament / traitement |

| Mouth |

La bouche |

| Muscle |

Le muscle |

| Nausea |

la nausée |

| Neck |

Le cou |

| Nightdress |

Chemise de nuit |

| Nose |

Le nez |

| Nurse |

Infirmière |

| Operating theatre |

Bloc opératoire |

| Operation |

Intervention chirurgicale |

| Operation |

Intervention |

| Out of breath |

essoufflé |

| Pain killer |

Calmant |

| Paramedics |

SAMU |

| Permission to operate |

Autorisation d’opérer |

| Physio after an accident |

Re-éducation |

| Physiotherapist |

Kinésithérapeute |

| Physiotherapy |

Kinésithérapie |

| Pill |

Cachet / Comprime |

| Pyjamas |

Pyjama |

| Rib |

La côte |

| Scratch |

une égratignure |

| Sensitive |

Sensible |

| Set up a drip |

Faire une perfusion |

| Shoulder |

L’épaule |

| Sleeping pill |

Somnifère |

| Slippers |

Pantoufles |

| Soap |

Le savon |

| Sore |

endolori |

| Spleen |

La rate |

| Sticking plaster |

Sparadrap / pansement adhésif |

| Stitches |

Points de suture |

| Stomach (external) |

Le ventre |

| Stomach (internal) |

L'estomac |

| Stretcher |

Brancard |

| Surgeon |

Chirurgien |

| Surgical dressing |

Pansement |

| Swelling |

une bosse |

| Swollen |

enfle |

| Take your blood pressure |

Contrôler votre tension |

| Teeth |

Les dents |

| Tender |

sensible |

| Tendon |

Le tendon |

| Thigh |

La cuisse |

| Throat |

La gorge |

| Thumb |

Le pouce |

| Tired |

fatigue |

| Toenail |

L'ongle du pied |

| Toes |

Les orteils |

| Tongue |

Le langue |

| Towel |

Une serviette |

| Ulcer |

ulcère |

| Water |

L'eau |

| Wheelchair |

Fauteuil roulant |

| Wounded |

blessé |

| Wrist |

Le poignet |

| X-ray |

Radio |

|

| rong>ENGLISHrong> |

rong>FRENCHrong> |

| Call an ambulance |

Appeler une ambulance |

| Call the emergency services |

Appeler le urgences |

| Call the police |

Appeler la police |

| Do not get up |

Ne pas se lever |

| Do you know an English speeking doctor? |

Connaissez-vous un médecin qui parle anglais? |

| Do you want an injection? |

Voulez-vous une piqûre? |

| I am allergic to… |

Je suis allergique a / a la / aux… |

| I am constipated |

Je suis constipé(e) |

| I am diabetic |

J'ai le diabète |

| I am going to faint |

Je vais m’evanouir |

| I am in pain |

J'ai mal |

| I am taking medication |

Je prends des médicament |

| I don't feel very well |

Je ne me sens pas tres bien |

| I feel better |

Je me sens mieux |

| I feel sick |

J'ai envie de vomir / J'ai mal au cœur |

| I feel bad |

Je me sens mal |

| I feel weak |

Je me sent faible |

| I feel worse |

Je me sens moins bien |

| I fell over |

Je suis tomber |

| I have a broken bone |

J’ai une fracture |

| I have a broken tooth |

J'ai une dent cassée |

| I have a chest cold |

J’ai une bronchite |

| I have a cold |

Je suis enrhumé |

| I have a cold |

J’ai une rhume |

| I have a got fever |

J’ai de la fievre |

| I have a headache |

J'ai mal à la tête |

| I have a sore throat / tonsilitis |